Oil shock could send Bitcoin down 45% if price surge forces Fed to delay cuts

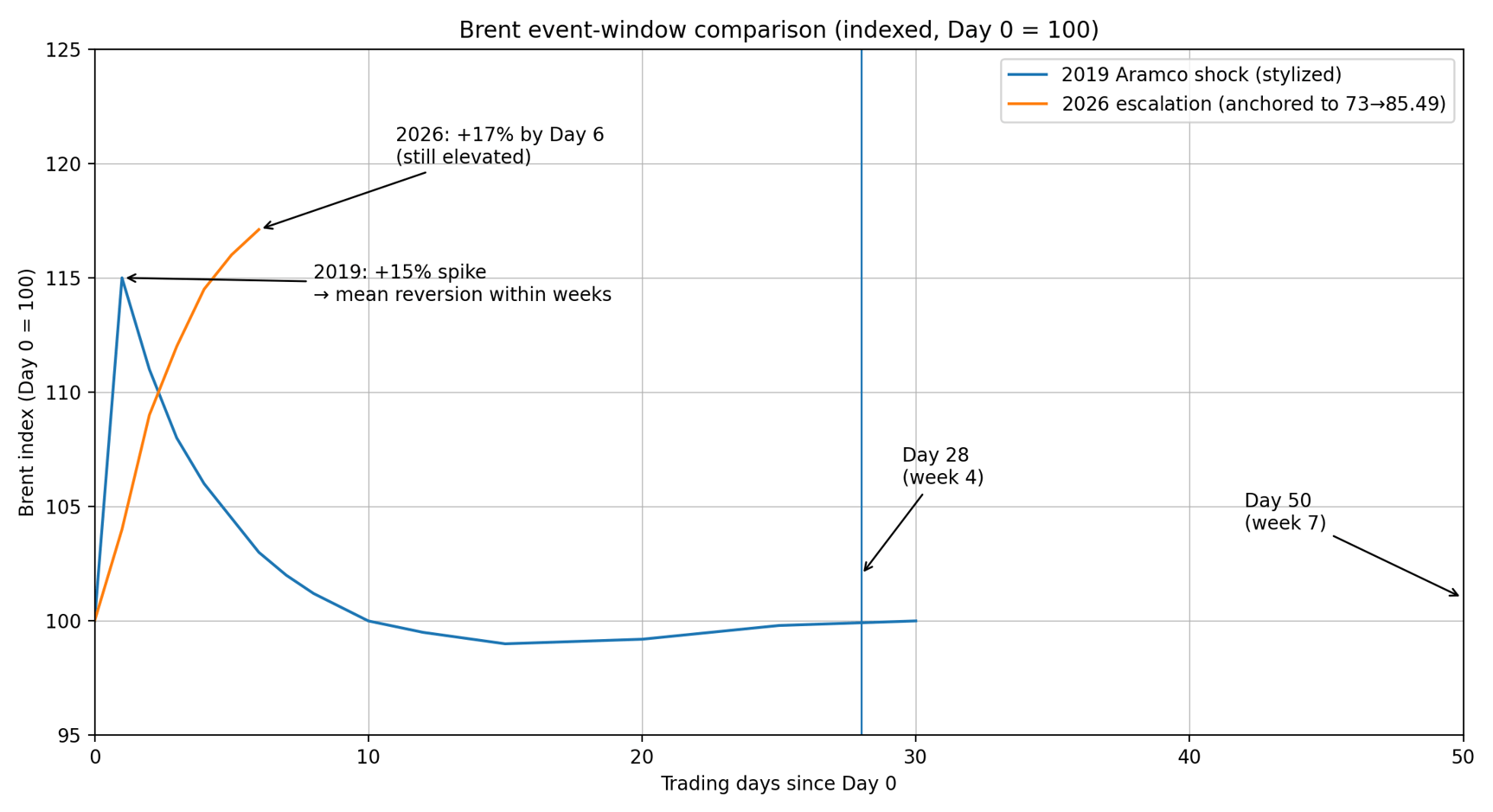

President Donald Trump projected four to five weeks for the conflict with Iran to come to an end. The market priced its playbook: headline shock, brief spike, diplomatic theater, then normalization.

That script worked in 2019 when drones hit Saudi Aramco facilities, and Brent jumped 15% only to surrender the entire gain within weeks. Traders bought the panic, sold the resolution, and moved on.

However, six days into the US/Israel-Iran escalation, Brent is at $85.49, up 17% from the $73 pre-strike anchor price. The question traders can’t answer is whether this resolves before week four or stretches past week seven.

That’s 50 days, the threshold where the nature of the shock fundamentally changes.

The distinction between a three-week disruption and a seven-week conflict matters more than the current price. Macquarie’s commodity desk frames the inflection cleanly: the global system absorbs a Hormuz disruption for one to two weeks without structural economic damage.

Pain accelerates past week three. Week four becomes the cliff where risk premium transforms into an inflation story that central banks can’t ignore.

By week seven, 50 days, the test is whether the Federal Reserve can deliver its projected June rate cut or must hold the line at 3.75% to prevent inflation expectations from breaking loose.

For Bitcoin, which has spent the past months riding the “Fed pivot” narrative as its primary bullish catalyst, the shift from a liquidity tailwind to a liquidity stall represents a headwind the asset has no mechanism to avoid.

The transmission mechanism no one wants to price

Oil moves through the Strait of Hormuz, channeling roughly 20% of global oil flows and a similar share of LNG. Geography converts regional conflict into a global supply constraint.

JPMorgan flags that a prolonged Hormuz closure threatens 3.3 million barrels per day, modeling how physical tightness translates into macro repricing that forces its way into central bank frameworks.

Asian refining margins telegraph the stress. Complex margins hit $30 per barrel, jet fuel cracks above $52, and gasoil above $48. These levels indicate refiners can’t source alternatives.

China asked refiners to halt export contracts and cancel shipments to protect domestic supply amid a spike in wholesale prices. Diesel jumped 13.5% in one week, gasoline 11%.

Japan’s refiners requested access to strategic stockpiles even as officials signaled that no immediate release was planned. The request shows actors with physical exposure pricing the possibility that this extends long enough to strain inventories.

Duration rewrites impact. A $10 spike reversing in 10 days is noise. A $15 move persisting 50 days forces into inflation prints, into expectations surveys central banks monitor, into the rate path governing system liquidity.

Allianz quantifies the threshold: beyond four to six weeks, implications compound. At three months, recession risk shifts from tail to base case.

Every 10% sustained oil move adds 0.1 to 0.2 percentage points to CPI. Pushing Brent from $73 to $100 is equivalent to a half-point inflation impulse, keeping the Fed at 3.75% through 2026 and abandoning the June cut.

What $100, $125, and $150 actually mean

Markets don’t need to speculate. Multiple banks have stress-tested the scenarios, their price targets mapping to escalating economic damage.

At $100, Brent jumps 37% above the $73 baseline, and the scenario is in prolonged-disruption territory, where the risk premium persists without collapsing the economy.

Goldman Sachs modeled this as a severe case. Allianz uses it as the threshold where Fed cuts evaporate.

From today’s $85.49, $100 would require an 18.6% increase, which is plausible if Hormuz remains contested or if infrastructure damage compounds shipping constraints.

That level implies 37% crude climb from baseline, generating a 0.5 to 0.7 percentage-point inflation impulse. The Fed’s 2026 easing path rests on inflation grinding toward 2%.

A half-point shock doesn’t permanently break that, but delays cuts from June to the fourth quarter, or eliminates them if oil stays elevated through summer.

At $120 to $150, framing shifts from “inflation complication” to “growth threat.” Bernstein discussed this as an extreme, prolonged conflict in which infrastructure is targeted and shipping adapts slowly.

At $125 Brent, up 48.2%, the inflation impulse climbs to 0.8-1.6 percentage points. Economists deploy “meaningful drag” and “material damage.” Earnings forecasts get revised down. Equities reprice as discount rates move against risk assets.

Bitcoin accelerates that repricing, trading as levered beta to liquidity.

At $150, it’s a recession prep. The 77.9% move implies 1.3 to 2.6 percentage points added to CPI. Central banks debate whether to hike into a slowdown to prevent unanchoring.

The 2008 oil spike to $147 preceded easing only after crude collapsed, and the crisis forced central banks’ hands. Initial response to $140+ was tightening bias.

Bitcoin gets repriced as high-beta risk, with no cash flows and no anchor beyond liquidity conditions.

| Brent scenario | % vs $73 baseline | % vs $85.49 today | CPI impulse range* | Macro / Allianz-style framing | Goldman Sachs / BTC framing |

|---|---|---|---|---|---|

| $100 | +36.99% | +16.97% | +0.37 to +0.74pp | Prolonged disruption; cuts delayed / at risk | “Higher-for-longer” repricing; BTC -5% to -15% |

| $125 | +71.23% | +46.22% | +0.71 to +1.42pp | Macro-relevant inflation impulse; growth drag starts | Risk de-rating; BTC -15% to -35% |

| $150 | +105.48% | +75.46% | +1.05 to +2.11pp | Recession-risk regime; policy dilemma | Forced de-risking; BTC -25% to -45% |

Bitcoin’s problem isn’t oil

The line from oil to Bitcoin runs through inflation expectations and monetary response. When Brent stays elevated, inflation prints rise.

When inflation rises, central banks delay easing or hold rates higher. When rates stay higher, risk assets face valuation headwind, and the opportunity cost of holding volatile, zero-yield instruments increases.

Academic work finds that a one-basis-point tightening shock to short rates corresponds to roughly a 0.25% move in Bitcoin. Not a law, but a sensitivity estimate that provides the scaffold for modeling what 50 days of elevated oil do.

If Brent averages $95 to $105 through week seven, you’re in “cuts postponed.” The Fed holds, real yields grind higher. Bitcoin faces 5% to 15% headwind as liquidity expectations reprice.

If Brent averages $100 to $110, you’re in Allianz’s “no 2026 cut” world. Long-end yields reflect higher-for-longer. Bitcoin, behaving like a levered tech stock when liquidity tightens, sees a 10% to 25% drawdown.

If Brent tests $120 to $150, you’re in forced de-risking. Recession talk enters discourse. Volatility spikes across assets. Bitcoin doesn’t rally on inflation-hedge narrative—it sells with everything else, down 25% to 45%.

The overlooked second channel: miner economics

Oil moves electricity costs, and electricity costs govern miner profitability. VanEck flags breakeven thresholds: older rigs like the S19 XP become uneconomic above roughly $0.07 per kilowatt-hour before overhead or depreciation.

When energy prices surge, miners sell Bitcoin to cover costs or shut down capacity. Either price pressure, sell-off, or reduced network security.

This channel moves more slowly than rates but compounds over the course of weeks. A 50-day war tests whether miners in expensive-power regions stay online and whether sell pressure builds while macro attention fixates on inflation.

What does week four actually tests

The market doesn’t need $150 oil to hurt Bitcoin. It needs oil elevated enough and sustained long enough to rewrite the assumptions baked into rate expectations and liquidity forecasts.

Week four is where Macquarie says the pain “definitely” accelerates.

Week seven puts the oil price past every threshold where banks model “manageable” and into the zone where macro damage becomes the baseline assumption.

Trump said four to five weeks. If he’s right, Brent returns to $80, inflation fears fade, and the Fed’s June cut stays on the table. Bitcoin trades in the relief rally as liquidity expectations stabilize.

However, if the conflict extends to 50 days, the scenarios stack differently. At $100 Brent, the no-cut case is tested. At $125, the test is on pricing recession risk. At $150, there is no test, the market is already there.

Bitcoin doesn’t control oil. It doesn’t control the Fed. What it does is reflect the liquidity regime that those forces create.

And when a conflict that was supposed to last weeks stretches into its seventh, the regime shifts from “easing ahead” to “higher for longer.” That shift is the headwind no volatility surface can hedge.

The post Oil shock could send Bitcoin down 45% if price surge forces Fed to delay cuts appeared first on CryptoSlate.